Maryland Gov. Wes Moore recently signed the Gift Card Scams Prevention Act of 2024, creating the country’s first law aimed at curbing a rising form of gift card fraud called card draining.

Card draining is a scheme in which thieves remove gift cards from stores, capture their numeric codes or swap them out for counterfeit cards, and place the products back on display. When an unsuspecting customer loads money onto a tampered or counterfeit card, criminals access it online and steal the balance.

The Maryland law marks a milestone in the growing government effort to combat card draining, which escalated dramatically during the pandemic thanks to the ingenuity of Chinese organized crime rings. ProPublica recently reported that late last year, after a spate of consumer complaints and arrests, the Department of Homeland Security launched a task force to address card draining.

“We’re talking hundreds of millions of dollars, potentially billions of dollars, [and] that’s a substantial risk to our economy and to people’s confidence in their retail environment,” Adam Parks, a Homeland Security assistant special agent in charge, told ProPublica.

The Maryland law is the first in the nation to mandate secure packaging for most gift cards sold in person. The bill’s packaging requirements sparked industry pushback that at one point threatened the bill’s passage, according to Sen. Ben Kramer, the Maryland state senator who sponsored the legislation.

Here’s how the battle unfolded, who was involved and why the Maryland bill is poised to change gift card packaging nationwide.

The Card-Draining BoomWhen big box retailers and pharmacies remained open during pandemic lockdowns, criminals saw that stores displayed hundreds of gift cards with little or no supervision. Crooks affiliated with Chinese organized crime began stealing unloaded cards and learned to remove and replace the security stickers and packaging that conceal card codes.

“It gave a lot of time and opportunity for people to figure out the flaws” in card security, said Jordan Hirschfield, who covers the prepaid card industry for Javelin Strategy & Research.

An estimated $570 billion is loaded onto gift and prepaid cards each year in the United States, Hirschfield said. While it’s difficult to know how much of that money has been stolen, even a 1% fraud rate would result in $5.7 billion in annual consumer losses, according to Hirschfield’s data.

One quarter of U.S. respondents said they had given or received a card with no balance, presumably because it had been stolen, according to a 2022 survey of about 2,000 adults by the AARP, the nonprofit advocacy group for people over age 50.

Hirschfield and law enforcement say that “open-loop” gift cards are particularly popular with draining gangs. Such cards use the Visa, Mastercard or American Express networks and can be spent at any business that accepts debit payments. They’re more versatile than “closed-loop” gift cards, which can be spent only at a single business, such as Target or Applebee’s.

Among other measures, Kramer’s bill required open- and closed-loop cards purchased in person to be sold in secure packaging that conceals their codes and shows signs of tampering when opened.

Citing a rise in consumer complaints and lawsuits, Kramer told ProPublica that the legislation was needed to protect consumers.

“This has been going on for several years now, and the industry was not addressing it,” Kramer said.

How Did the Industry React?Kramer’s bill elicited almost instant industry pushback.

“Clearly all hell broke loose within the industry,” he told ProPublica. “At first everybody was just trying to discourage me from doing anything.”

Lobbyists from Walmart, Target and Home Depot contacted Kramer, as did companies that manufacture gift cards and stock them in retail stores, including Blackhawk Network. Kramer said that new card packaging would cost companies money to design and manufacture.

Eventually, many national retailers and manufacturers came together through the Maryland Retailers Alliance to advocate for amendments, including allowing businesses to forgo the new packaging rules if their closed-loop gift cards are stored in a secure location accessible only to employees.

Then a lobbyist for InComm Payments, a payments technology provider that manages gift card programs for major retailers, asked the committee to change the open-loop card requirements. The lobbyist proposed removing the bill’s reference to “secure packaging” and eliminating the requirement that open-loop cards conceal their activation codes. Along with managing card programs for partners including Walmart and CVS, InComm, via a subsidiary, sells its own popular line of Vanilla open-loop gift cards.

The company’s amendment would have gutted a major protection against card draining, according to Kramer. InComm “was trying to scuttle the bill,” he said.

InComm said its proposed changes were intended to give companies the flexibility to adapt card packaging in order to combat new fraud techniques. It added that it proposed removing the bill’s reference to secure packaging because the bill’s language “was not fully reflective of industry security best practices.”

“To be absolutely clear, all of our lobbying engagement related to the Maryland bill had the end-goal of empowering the industry to implement the most impactful secure packaging techniques that are in the best interest of consumers — now and in the future,” the company said in an emailed statement.

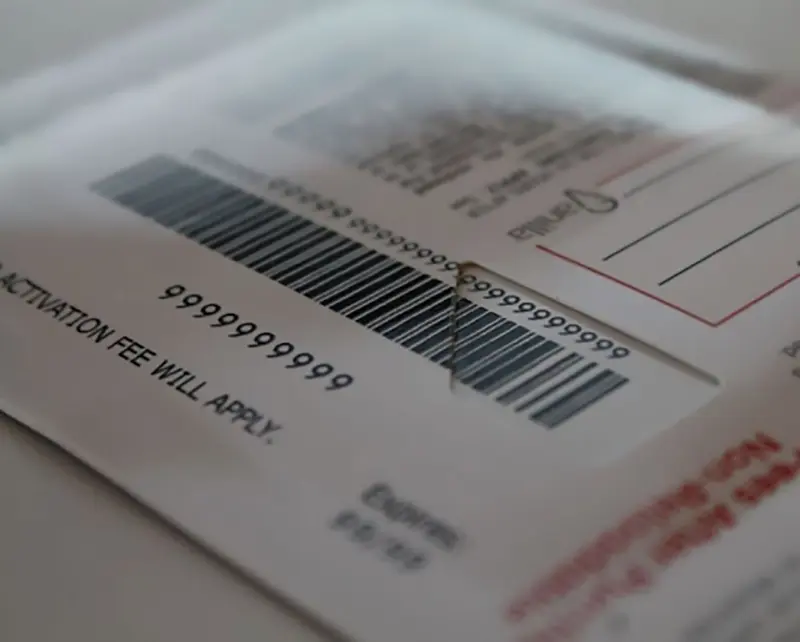

InComm’s proposed amendment kicked off what would become a key point of conflict: how to display activation codes.

A gift card’s activation code is scanned at the point of sale to turn on the card and load its cash balance. It’s different from a redemption code, PIN or CVV, which are used when a customer uses a card to make a purchase. InComm, the Maryland Retailers Alliance and Kramer all agreed that redemption data and related codes should be fully concealed. But InComm argued that activation codes didn’t need to be fully covered to prevent fraud.

InComm patented a type of packaging in 2017 that prints the activation code across both the packaging and the card. The company said in a statement to ProPublica that this method, which it calls split-barcode packaging, is more secure than fully covering an activation code.

“If attempts to tamper cause the card and external barcode to become misaligned by a fraction of a millimeter, it prevents the barcode from being scanned and activated,” the company said.

InComm declined to say what percentage of Vanilla cards use split barcode packaging but said that “every Vanilla Gift Card released in 2024 has new and innovative security enhancements included.”

InComm and Card DrainingThe jockeying over the Maryland bill came as InComm is facing government scrutiny over card draining.

Last November, David Chiu, the city attorney of San Francisco, filed a suit against the company’s card division, InComm Financial Services, and three of its banking partners alleging that InComm has been aware of card draining for roughly a decade and showed negligence by not fixing Vanilla packaging and by failing to refund consumers.

“InComm is selling these prepaid gift cards that it knows are susceptible to rampant theft due to inadequate packaging and security,” Chiu told ProPublica and alleged in the complaint.

InComm Payments said it “vigorously denies the baseless claims” in the San Francisco city attorney's lawsuit. It filed a motion in May to dismiss the case, saying the California court lacked jurisdiction over the company, which is registered in South Dakota. Three of its banking partners similarly moved to dismiss the claims against them. A California Superior Court judge is slated to meet with attorneys in September.

The lawsuit caught the attention of a federal lawmaker, Sen. Richard Blumenthal, D-Conn. In December, he asked the Federal Trade Commission to investigate InComm Financial Services, charging that its alleged “neglect and refusal to implement improved security features have unjustly harmed consumers.” (An FTC spokesperson said it “can neither confirm nor deny the existence of any investigation” into InComm.)

“I remain concerned that fraudsters are continuing to take advantage of InComm’s lacking security features of their prepaid gift cards — ultimately inflicting financial harm on consumers across the country,” Blumenthal said in a statement to ProPublica.

The company said it is not currently the subject of a memorandum of understanding, consent decree, or cease-and-desist from any regulator. It declined to say whether it had been contacted by the FTC in the past year or if it is currently the subject of an investigation from a government body.

“InComm Payments has been at the forefront in developing innovative solutions to continuously combat emerging fraud threats over the past 30 years, and maintains that vigilance today by leveraging new technologies, packaging techniques, monitoring systems and other security practices to help protect consumers,” the company said.

The Maryland Bill Becomes LawAs Kramer’s gift card bill advanced through the Maryland legislature, another industry trade group, the Retail Gift Card Association, floated a new proposal: allow the state attorney general’s office to decide whether a company’s packaging was sufficiently secure.

Three days later, InComm proposed a new amendment to allow activation data to be revealed if the packaging “is more secure than it otherwise would be if the data were fully concealed.”

Both ideas resonated with state Del. C.T. Wilson, the chair of the House Economic Matters Committee, who examined InComm’s packaging design.

“It's not that I was totally convinced that the thing that they showed me was the silver bullet. It definitely wasn’t,” he said. “But what I did not want to do was stop people from looking for more ways to secure the system.”

Wilson incorporated language from InComm’s amendment and added oversight by the state attorney general’s office. The bill passed in April.

The new packaging rules take effect next June, so companies have a year to come into compliance. While the law applies only to cards sold in Maryland, it’s likely the packaging changes will be rolled out nationwide because companies prefer to use the same cards across all states, according to Kramer and Cailey Locklair, the president of the Maryland Retailers Alliance.

“It will change packaging nationally — it is not just a Maryland bill,” Locklair said. She predicted the new packaging will begin appearing in stores by the holidays, typically the peak time for card draining.

A Blackhawk spokesperson declined to comment on any packaging changes it plans to make but said the company “will comply with any and all legislative requirements.” InComm also declined to share details on potential packaging changes, saying it wanted to avoid aiding criminals. But it said its split-barcode packaging “fully complies with the Maryland law.”

“I think of a bill like this as the first domino” in combating gift card fraud, Kramer said, adding, “I think we ended up with a great consumer protection bill.”

ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up to receive our biggest stories as soon as they’re published.

ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up to receive our biggest stories as soon as they’re published.